One of my favorite musical artists is John Prine. We lost him earlier this year, another Covid victim. The first song on his first album is titled Illegal Smile. It describes the plight of a fellow who is down on his luck and what he does to compensate. In one lyric, he learns that “All my friends turned out to be insurance salesmen.” That statement sums up what many people think about insurance, and insurance salesmen – not too popular.

So, when someone tells you that you should get some insurance, it’s easier to think about the money you’re giving up, instead of what you might save, in the event something bad happens. We can choose to take steps now, some costly ones, to help avoid the future impacts of climate change; or we can continue to pay for the inevitable future repair work – e.g., rebuilding after hurricanes or floods or wildfires. Like an insurance policy, can we consider spending money now to mitigate climate change later?

Many communities across the country are already taking steps, costly ones, to mitigate the effects of future floods and rising sea levels. Zoning laws are changing for future structures and land use – all positive actions to reduce the anticipated impacts associated with climate change. And while building higher sea walls and raising home foundations are good, and necessary, these steps do not address the root causes of climate change. They are like applying band-aids to injuries instead of changing the way we live by addressing the things that are causing climate change.

The outcome of the upcoming presidential election will have a significant impact on whether or not the United States makes substantial investments to address climate change. The New York Times recently published a story, The Election and Climate Change, which details the positions of both candidates.

President Trump has never issued, nor does he have, a plan for climate change. If reelected, he will likely continue to deny that climate change is a result of human activity – rather, he will likely say it is a hoax, possibly a conspiracy theory. In a second term, some advances in renewable energy (solar, wind) will be made, but Trump will likely continue to be a strong advocate for the fossil fuel industry and continue his assault on regulations to protect the environment – arguing they are “job killers”.

In contrast, former Vice-President Biden, if elected, has proposed the most ambitious climate action plan ever presented by a presidential nominee of a major party. His plan is for the United States to zero out greenhouse-gas emissions by 2050, and he has proposed spending $2 trillion over four years as a starting point. He has focused on the health and economic benefits — cleaner air, and the creation of new industries. The policy of a Biden administration would reinstate regulations protecting the environment that have been eliminated or weakened by Trump. (Read the details in the links.)

But, is it worth $2 trillion over the next four years? Certainly, that question will be heavily debated before new laws or appropriations to implement these expenditures are enacted. If we think about these expenditures as “insurance” against potential future losses, how do we decide if we should “buy the insurance” or “skip the insurance and take our chances”? In other words, are we getting our money’s worth by addressing the root causes of climate change or would we be better off not buying this “insurance” and instead, continue to spend money to fix the damages?

The federal government’s National Climate Assessment warns that even moderate warming could cost the American economy hundreds of billions of dollars each year by century’s end. For example, we’ll have deadlier heat waves, crop failures, more destructive wildfires and higher sea levels and all of these events will cost us more than we’re spending now.

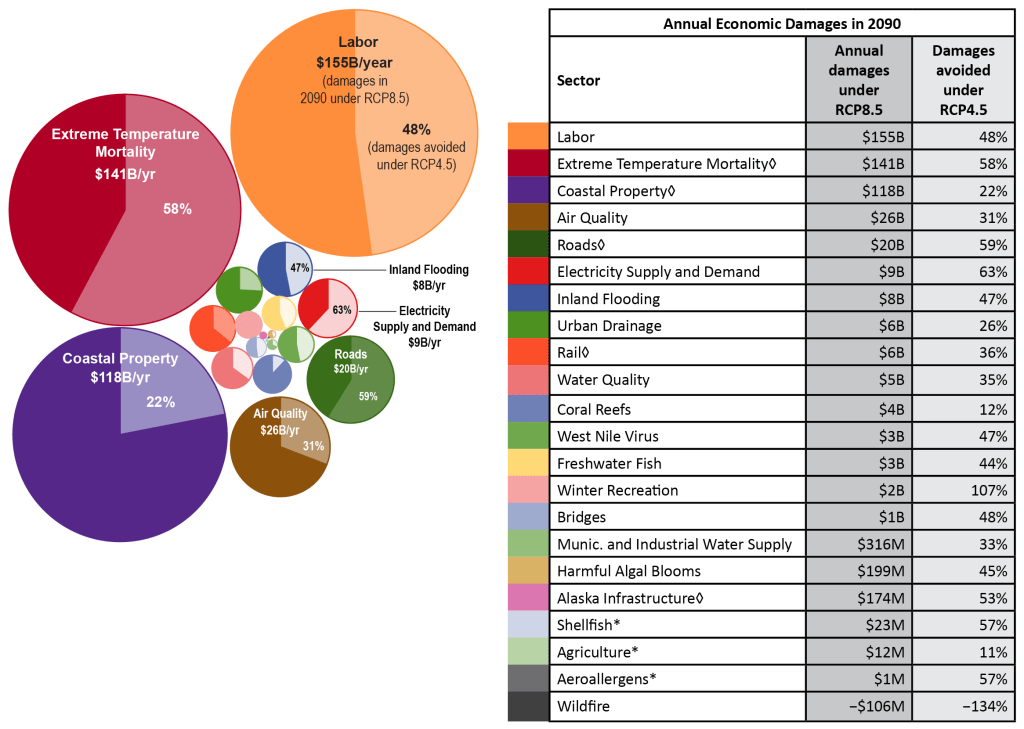

Representative Concentration Pathway, “RCP” notation, describes different levels of greenhouse gas concentration and is used to model future climate scenarios. The chart below provides a comparison of annual economic damages under two scenarios, noted as RCP 8.5 and RCP 4.5. In RCP 8.5 – considered a worst-case – emissions continue to rise throughout the 21st century. RCP 4.5 assumes that carbon dioxide (CO2) emissions start declining by approximately 2045 to reach roughly half of the levels of 2050 by 2100.

Similarly, studies have been conducted that estimate the annual change in the economy over time as a result of climate change. The growth in our economy is typically discussed in terms of a year-over-year percent change in our Gross Domestic Product (GDP). For example, the change in our GDP in 2018 was 2.93%. In 2019, it was 2.33% and in 2020, it is estimated to be negative 5.91%. In other words, not surprisingly, our economy contracted, rather than expanded in 2020, as a result of Covid-19 and the associated economic inactivity within our country.

Having endured the economic hardships of these past months, most people understand how a negative growth in GDP feels – awful. With climate change, it will be worse. A group of over 1000 economic experts were surveyed regarding the long-term economic impact that climate change will cause. More than three-quarters of respondents believe that climate change will have a long-term, negative impact on the growth rate of the global economy. Economic experts predicted far higher economic impacts from climate change than previous surveys of economists and other climate experts. Respondents predicted a global GDP loss of roughly 10% if global mean temperature increases by 3°C, relative to the pre-industrial era, by 2090. This increase assumes a “business as usual” emissions scenario. That’s almost double the negative economic impact that Covid has caused. And many of these respondents believe that there is greater than a 20% likelihood that this same climate scenario would lead to a “catastrophic” economic impact, defined as a global GDP loss of 25% or more.

So, it’s fair to say over the long term, most economic experts believe climate change will have devastating impacts on our economy. Now with all of these estimates of future costs, one may think we can simply “do the calculations” and see if the payoff on what we need to spend now is worth the future savings. This is the approach we would typically do when considering whether or not to buy some “insurance” – is the cost now worth the future risk of loss? These types of questions will likely be debated as initiatives are proposed to mitigate the impacts of climate change.

I believe this is a false choice. We cannot afford to risk destroying our planet. It is not a question of the “insurance cost”. Regardless of insurance, if your house burns down and you cannot rebuild, and there is no other place to go, no other place where you can live – you will be homeless, and defenseless. That’s what it will be like if our planet effectively “burns up” slowly, but continuously, so that, eventually, there will be no place to go that will be safe. If we burn up our planet, by failing to act before climate change becomes irreversible, we will be without a habitable home.

Margaret Renkl is a New York Times contributing opinion writer who covers flora, fauna, politics and culture in the American South. She recently wrote an article, I Am Watching My Planet, My Home, Die. In it, she makes the point that spending to address climate change is critical because we don’t have a “planet B” option and that all other important issues — education, social justice, women’s rights, affordable health care, criminal justice reform, gun control, immigration policy etc. — won’t mean a single thing if the planet becomes uninhabitable.

Margaret Renkl makes a good point! So does John Prine through his music catalogue!

Well done, Good guy!

LikeLiked by 1 person